Mortgagerateslocal.com – Understanding what sets mortgage rates is crucial for anyone looking to buy a home or refinance their existing mortgage. These rates determine the cost of borrowing and can have a significant impact on the affordability of homeownership. In this report, we will explore the various factors that influence mortgage rates and shed light on the complex dynamics behind their fluctuations.

Economic conditions play a pivotal role in determining mortgage rates. A thriving economy marked by low inflation, low unemployment rates, and steady GDP growth generally results in lower mortgage rates. This is because a strong economy provides lenders with confidence in borrowers’ ability to repay their loans. On the other hand, during times of economic uncertainty or recession, mortgage rates tend to decrease in order to stimulate borrowing and bolster the housing market.

Central bank policies are another key driver of mortgage rates. Central banks, such as the Federal Reserve in the United States, regulate short-term interest rates. Changes in these rates can indirectly impact long-term mortgage rates. When the central bank raises interest rates to curb inflation or slow down economic growth, mortgage rates tend to rise as borrowing becomes more expensive. Conversely, when the central bank lowers interest rates to encourage economic activity, mortgage rates often follow suit.

The bond market also exerts a significant influence on mortgage rates. Mortgage rates are closely tied to the yield on treasury bonds. When bond yields increase, mortgage rates tend to rise as well. This is because investors flock to the bond market when they expect higher returns, causing bond prices to fall and yields to rise. On the other hand, when demand for bonds increases, yields decrease, leading to lower mortgage rates.

The creditworthiness of borrowers is a critical factor that determines the interest rate offered on a mortgage. Lenders assess borrowers’ credit scores and debt-to-income ratios to gauge their ability to repay the loan. Borrowers with higher credit scores and lower debt burdens are considered less risky, allowing them to secure lower mortgage rates. Conversely, borrowers with poor credit histories or high levels of debt may be deemed higher risk and thus face higher interest rates.

Are Mortgage Rates the Same for All Lenders?

No, mortgage rates can vary among lenders. Each lender sets their own rates based on their assessment of the borrower’s risk and their business strategy. Various factors such as the lender’s cost of funds, overhead expenses, and desired profit margins can influence the rates they offer.

In addition to internal factors, different lenders may have access to unique loan programs or special offers, which can result in varying rates. To find the most favorable mortgage rate for your financial situation, it is crucial to shop around and compare rates from multiple lenders.

When it comes to securing the best mortgage rate, conducting thorough research and shopping around is essential. By exploring multiple lenders and understanding the various factors that influence rates, you have a better chance of finding a competitive rate that aligns with your needs.

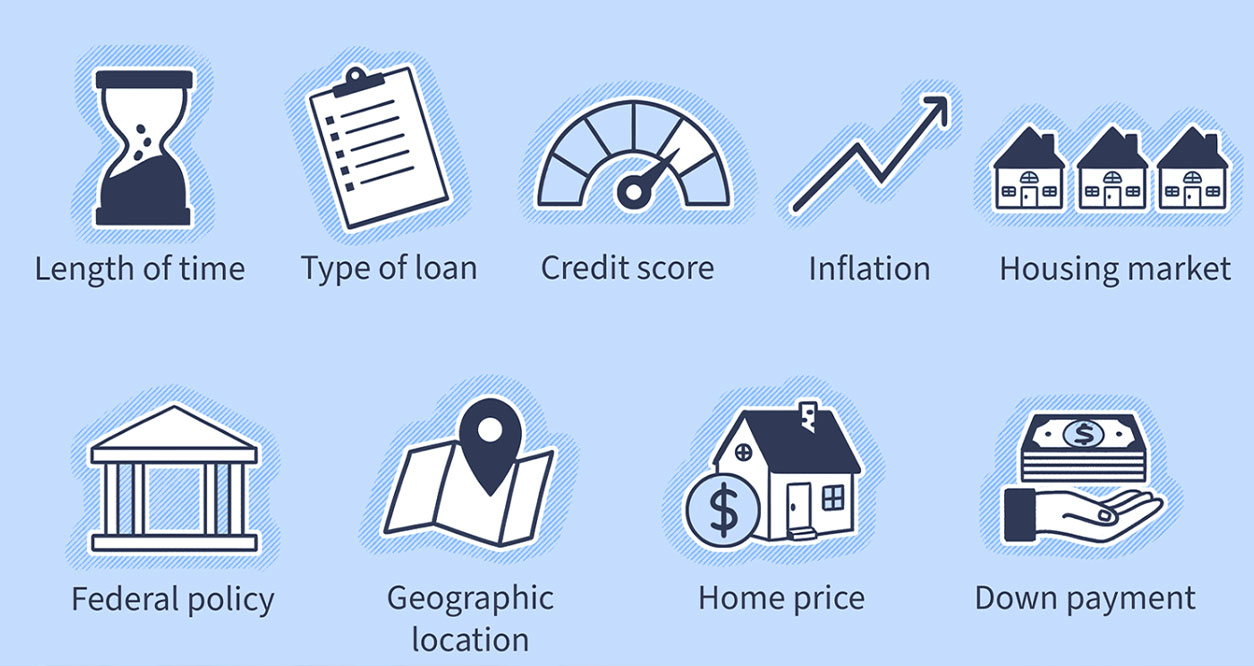

What Sets Mortgage Rates?

Mortgage rates can vary between different lenders and can also fluctuate over time. Lenders take into account various factors when setting mortgage rates, including economic conditions, loan terms, borrower qualifications, and market trends. Let’s take a closer look at each of these elements:

1. Economic Conditions and Monetary Policy

The state of the economy and the monetary policy adopted by the central bank play crucial roles in determining mortgage rates. When the economy is thriving, with low unemployment rates and steady economic growth, mortgage rates tend to rise. This is because lenders perceive less risk in lending during favorable economic conditions. Conversely, during times of economic uncertainty or recession, mortgage rates tend to decrease. This decrease aims to stimulate borrowing and boost the housing market during challenging economic times. The central bank’s monetary policy decisions, including adjustments to interest rates, also impact mortgage rates. A decrease in the central bank’s interest rates can result in lower mortgage rates, making borrowing more accessible and affordable for homebuyers.

Additionally, inflation levels also influence mortgage rates. Lenders must take inflation into account when setting mortgage rates, as inflation erodes the purchasing power of money over time. Consequently, when inflation is high, lenders may increase mortgage rates to mitigate the risk of inflation eroding the value of the loan over the loan term.

2. Loan Terms and Features

The terms and features of your mortgage play a crucial role in determining the mortgage rates you’re offered. Some key factors to consider include the loan term, the down payment amount, and the type of interest rate. Mortgage terms typically range from 15 to 30 years, with shorter terms generally offering lower interest rates. This is because shorter-term loans present less risk to lenders, resulting in lower rates. Making a larger down payment can also lead to more favorable mortgage rates as it reduces the lender’s risk. Additionally, choosing between a fixed-rate or an adjustable-rate mortgage can affect your mortgage rates. Fixed-rate mortgages offer stable and predictable payments, while adjustable-rate mortgages may start with lower rates but can fluctuate over time.

Lenders also consider the loan-to-value ratio (LTV) when determining mortgage rates. The LTV ratio is the loan amount divided by the appraised value of the property. A higher LTV ratio represents a higher risk for the lender, leading to higher mortgage rates.

3. Borrower Qualifications and Credit Score

Your personal financial situation significantly impacts the mortgage rates you’re eligible for. Lenders assess factors such as your credit score, income level, and debt-to-income ratio (DTI) to determine your creditworthiness. A higher credit score demonstrates responsible financial behavior, making you less risky to lenders. Consequently, borrowers with higher credit scores are often offered lower interest rates on their mortgage loans. It’s crucial to monitor and maintain a good credit score to access the most favorable mortgage rates. Lenders also prefer borrowers with stable income sources and a low DTI, as it indicates a lower risk of defaulting on the loan. If you have a poor credit score or unstable income, you may be offered higher mortgage rates or face difficulties in obtaining a mortgage.

Furthermore, the size of your mortgage loan and the amount of your down payment can affect the interest rates offered. Jumbo loans, which exceed the conforming loan limits set by government-sponsored enterprises like Fannie Mae and Freddie Mac, often have higher interest rates due to the increased risk associated with larger loan amounts.

4. Job Growth

The health of the job market is another external factor that affects mortgage rates. Job growth and unemployment rates impact consumer spending and overall economic stability. When job growth is strong, and unemployment is low, mortgage rates may rise due to increased demand and higher competition among borrowers.

Conversely, during periods of limited job growth or high unemployment rates, mortgage rates may decrease to encourage borrowing and stimulate economic activity. It’s crucial to consider the job market conditions when planning to purchase a home or refinance your existing mortgage.

5. Market Trends and Competition

The mortgage market is influenced by prevailing market trends and competition among lenders. Mortgage rates can fluctuate based on changes in supply and demand for mortgage loans. When housing demand is high, lenders may increase rates to match the increased demand. Conversely, during periods of lower demand, lenders may lower rates to attract borrowers. It’s crucial to keep an eye on market trends and compare rates from multiple lenders to ensure you’re getting the most competitive mortgage rates available.

FAQ

The Federal Reserve, also known as the central bank of the United States, has a significant impact on mortgage rates. One of the main tools the Federal Reserve uses to influence mortgage rates is the adjustment of the federal funds rate. Changes in the federal funds rate can indirectly affect mortgage rates, as it influences the rates banks charge one another for short-term borrowing. Additionally, the Federal Reserve’s monetary policy decisions can also impact market conditions, which, in turn, affect mortgage rates.

Credit score plays a crucial role in determining mortgage rates. Lenders use your credit score as an indication of your creditworthiness. A higher credit score demonstrates responsible financial behavior, making you less risky to lenders. Consequently, borrowers with higher credit scores are often offered lower interest rates on their mortgage loans. It’s important to monitor and maintain a good credit score to access the most favorable mortgage rates.

The length of your mortgage term and the interest rate are closely related. Generally, shorter-term mortgages, such as 15-year loans, have lower interest rates compared to longer-term mortgages, such as 30-year loans. This is because shorter-term loans present less risk to lenders, resulting in lower rates. However, it’s crucial to consider your financial goals and budget when choosing a mortgage term, as shorter terms may come with higher monthly payments.

Yes, you can negotiate mortgage rates with lenders. While mortgage rates can vary between lenders, they are not set in stone. It’s always a good idea to shop around and compare rates from different lenders. You can use rate quotes from one lender as leverage to negotiate better rates with another lender. However, it’s important to keep in mind that your creditworthiness, loan terms, and market conditions will influence the rates you can secure.

Market conditions play a significant role in determining mortgage rates. Mortgage rates are influenced by factors such as supply and demand, economic indicators, and investor sentiment. During periods of economic stability and high demand for housing, mortgage rates tend to rise. Conversely, during times of economic uncertainty or low demand, mortgage rates often decrease. It’s essential to monitor market trends and work with a trusted lender who can advise you on the optimal timing for locking in your mortgage rate.

Conclusion

Thank you for taking the time to explore our comprehensive guide on what sets mortgage rates. Understanding the factors that influence mortgage rates is essential for anyone considering buying a home or refinancing their mortgage. By considering economic conditions and monetary policy, loan terms and features, borrower qualifications, and market trends, you can make informed decisions about your mortgage and secure the most favorable rates.