Mortgagerateslocal.com – Are you thinking of buying or selling a property with a loan? If so, you will need to know about mortgage deed format. A mortgage deed can secures the loan by giving the lender a claim on the property until the loan is paid off.

Mortgage deed is one of the most important documents in any real estate transaction, as it determines the rights and obligations of both the borrower and the lender. A mortgage deed can be of different types, depending on the nature and extent of the interest transferred to the lender.

Each type has its own advantages and disadvantages, and you should choose the one that suits your needs and preferences. But what exactly is a mortgage deed and what does it contain? How does it differ from other types of deeds?

We will answer these questions and more. We will explain the meaning, types, and key elements of a mortgage deed, and provide you with some tips on how to write one. By the end of this article, you will have a clear understanding of what a mortgage deed is and how it works.

What is a Mortgage Deed?

A mortgage deed, also known as a mortgage agreement or a deed of mortgage, is a written document that officially recognizes a legally binding relationship between a borrower and a lender. When a borrower takes out a loan to purchase a property, they agree to pay back the lender with interest over a period of time. To secure the loan, the borrower transfers an interest in the property to the lender. This interest is called a mortgage, and it allows the lender to recover the property if the borrower fails to pay.

A mortgage deed is the evidence of the interest transferred to the lender. It determines the terms and conditions of the loan, such as the amount, interest rate, repayment schedule, and consequences of default. It also specifies the rights and obligations of both parties, such as the borrower’s right to use and maintain the property, and the lender’s right to inspect and foreclose the property.

A mortgage deed is different from a deed of trust, which is another common type of document used to secure a loan. A deed of trust involves a third party, called a trustee, who holds the legal title to the property until the loan is paid off.

The trustee acts as an intermediary between the borrower and the lender, and has the power to sell the property if the borrower defaults. A deed of trust is more common in some states than others, and has some advantages and disadvantages over a mortgage deed.

Types of Mortgage Deeds

There are several types of mortgage deeds, depending on the nature and extent of the interest transferred to the lender. Some of the most common types are:

- Simple mortgage: This is the most basic type of mortgage deed, where the borrower transfers an interest in the property without delivering its possession. The borrower agrees to pay the loan amount with interest, and the lender has the right to sell the property if the borrower defaults.

- Mortgage by deposit of title deeds: This is a type of mortgage deed where the borrower deposits the title deeds of the property with the lender, without any written document. The deposit creates an implied contract between the parties, and the lender has the right to sell the property if the borrower defaults.

- Mortgage by conditional sale: This is a type of mortgage deed where the borrower transfers the property to the lender on the condition that the lender will return it to the borrower when the loan is paid off. The borrower retains the possession of the property, and the lender has the right to sell the property if the borrower defaults.

- Usufructuary mortgage: This is a type of mortgage deed where the borrower transfers the property and its possession to the lender. The lender has the right to use and enjoy the property, and to collect its rents and profits. The lender does not have the right to sell the property, and the borrower does not have the obligation to pay the loan.

- English mortgage: This is a type of mortgage deed where the borrower transfers the property and its possession to the lender, and agrees to pay the loan amount with interest on a fixed date. The lender has the right to sell the property if the borrower fails to pay on the due date.

- Anomalous mortgage: This is a type of mortgage deed that does not fall under any of the above categories, but is a combination of two or more types. For example, a mortgage deed that is partly a simple mortgage and partly a usufructuary mortgage.

Key Elements of a Mortgage Deed

A mortgage deed should contain the following key elements:

- The parties’ information: The names, addresses, and other identifying details of the borrower and the lender.

- The property details: A description of the property that is being mortgaged, including its location, size, value, and any encumbrances or liens on it.

- The loan amount and interest rate: The principal sum of the loan and the interest rate that the borrower has to pay to the lender.

- The repayment schedule: The dates and amounts of the payments that the borrower has to make to the lender, and the mode and method of payment.

- The default clause: The conditions and consequences of default, such as the lender’s right to foreclose the property, the borrower’s liability for any deficiency or surplus, and the costs and fees involved in the foreclosure process.

- The mortgage clause: The type and extent of the interest that the borrower transfers to the lender, and the rights and obligations of both parties regarding the property.

- The possession clause: The clause that states whether the borrower retains or delivers the possession of the property to the lender, and the terms and conditions of the possession.

- The insurance clause: The clause that states whether the borrower or the lender is responsible for insuring the property against any damage or loss, and the amount and coverage of the insurance.

- The acceleration clause: The clause that states whether the lender has the right to demand the full payment of the loan before the due date, in case of any breach or default by the borrower.

- The due-on-sale clause: The clause that states whether the borrower has the right to sell or transfer the property to another person, and whether the lender has the right to approve or reject the sale or transfer, or to demand the full payment of the loan upon the sale or transfer.

- The general clauses: The clauses that cover the general aspects of the contract, such as the governing law, the dispute resolution mechanism, the amendment and modification procedure, the severability and waiver provisions, and the signatures and witnesses.

How to Write a Mortgage Deed

Writing a mortgage deed can be a complex and tedious task, as it involves a lot of legal and technical terms and details. However, with some guidance and research, you can write a mortgage deed that is clear, accurate, and enforceable. Here are some steps that you can follow to write a mortgage deed:

- Step 1: Gather the information. Before you start writing, you need to gather all the relevant information about the parties, the property, the loan, and the mortgage. You can use online sources, public records, or professional services to obtain the information. You also need to check the laws and regulations of your state or jurisdiction, as they may vary from place to place.

- Step 2: Choose the format. You can use a template or a sample mortgage deed to guide you in writing your own. You can find many templates and samples online, or you can consult a lawyer or a real estate agent for assistance. You can also create your own format, as long as it covers all the key elements and follows the legal requirements of your state or jurisdiction.

- Step 3: Write the introduction. The introduction of the mortgage deed should state the date and place of the contract, and the names and addresses of the parties. It should also state the purpose and the consideration of the contract, and the recitals or the background information of the transaction.

- Step 4: Write the body. The body of the mortgage deed should contain all the key elements that we discussed above, such as the property details, the loan amount and interest rate, the repayment schedule, the default clause, the mortgage clause, the possession clause, the insurance clause, the acceleration clause, the due-on-sale clause, and the general clauses. You should use clear and precise language, and avoid any ambiguity or inconsistency. You should also use headings and subheadings to organize the content and make it easy to read and understand.

- Step 5: Write the conclusion. The conclusion of the mortgage deed should state the acknowledgment and agreement of the parties, and the signatures and witnesses of the parties. It should also state the date and place of the execution of the contract, and the seals and stamps of the parties, if applicable.

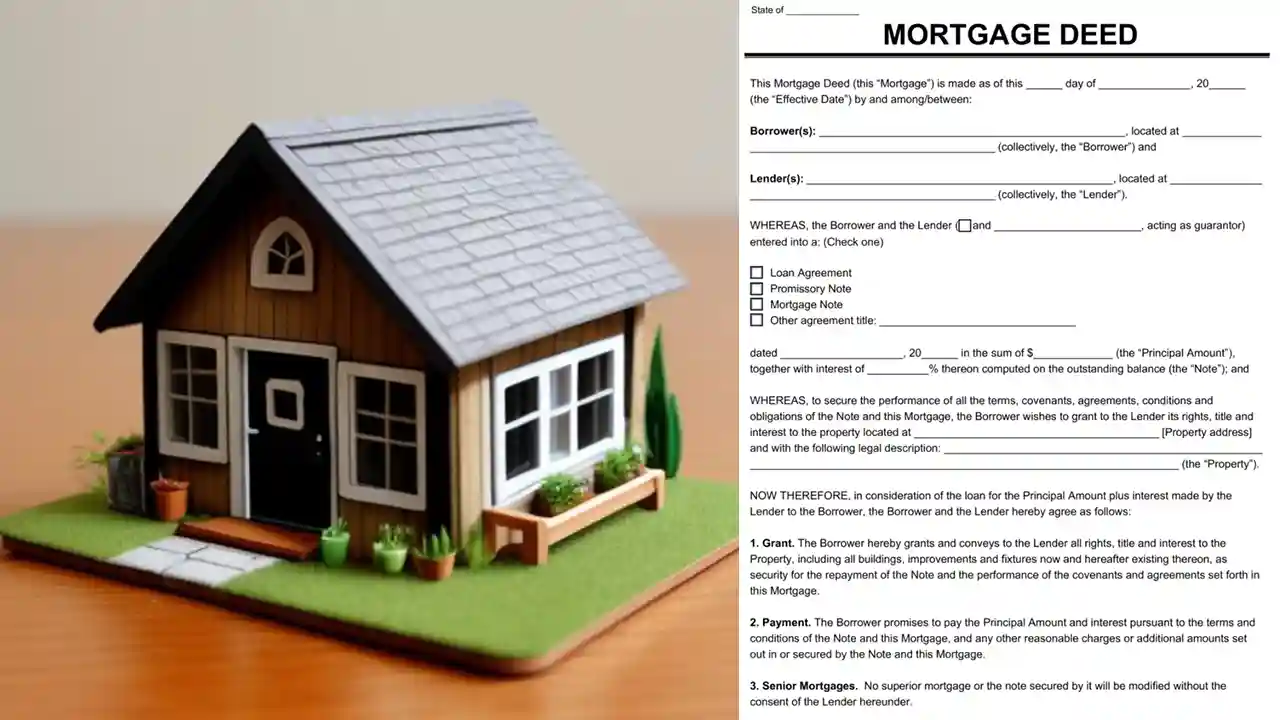

Sample Mortgage Deed

A sample mortgage deed is an example of a legal document that shows how a borrower and a lender can agree on the terms of a loan secured by a property. A sample mortgage deed can help you understand the format, structure, and content of a real mortgage deed that you may need to use or sign when buying or selling a property with a loan.

This Mortgage Deed is made on October 25, 2023, by and between John Smith, of 123 Main Street, Springfield, IL 62701, as the Borrower, and ABC Bank, of 456 Market Street, Springfield, IL 62702, as the Lender.

WHEREAS, the Borrower has obtained a loan from the Lender in the amount of $200,000, with an interest rate of 5% per annum, payable in monthly installments of $1,073.64 for 30 years, as evidenced by a promissory note dated October 25, 2023 (the “Note”);

WHEREAS, the Borrower has agreed to secure the repayment of the loan by granting a mortgage on the real property described below to the Lender;

NOW, THEREFORE, for good and valuable consideration, the receipt and sufficiency of which are hereby acknowledged, the Borrower hereby mortgages, grants, and conveys to the Lender, with power of sale, the following real property, together with all the improvements, fixtures, and appurtenances thereon or thereto belonging (the “Property”):

Lot 12, Block 34, Springfield Heights Subdivision, as per plat thereof recorded in Plat Book 12, Page 34, of the Public Records of Sangamon County, Illinois.

The Borrower covenants and agrees with the Lender as follows:

- The Borrower will pay the principal and interest of the loan according to the terms of the Note, and will pay all other sums that may become due under this Mortgage Deed or any other instrument executed in connection with the loan.

- The Borrower will pay all taxes, assessments, charges, and liens that may be levied or imposed on the Property, and will provide the Lender with evidence of such payments upon request.

- The Borrower will keep the Property in good repair and condition, and will not commit or permit any waste, damage, or deterioration of the Property.

- The Borrower will maintain adequate insurance on the Property against fire, casualty, and other risks, in an amount and form acceptable to the Lender, and will name the Lender as a loss payee on the insurance policies. The Borrower will promptly pay the premiums for the insurance and will deliver the policies and receipts to the Lender. The Borrower will notify the Lender of any loss or damage to the Property and will assign the proceeds of the insurance to the Lender, at the Lender’s option, to be applied to the loan or to the restoration of the Property.

- The Borrower will comply with all laws, ordinances, regulations, and restrictions that may affect the Property or the use and occupancy thereof, and will not use or permit the use of the Property for any illegal or immoral purpose.

- The Borrower will defend the title to the Property against all claims and demands, and will promptly notify the Lender of any suit, action, or proceeding that may affect the Property or the Lender’s interest therein.

- The Borrower will not sell, transfer, lease, encumber, or otherwise dispose of the Property or any part thereof, or any interest therein, without the prior written consent of the Lender. The Lender may, at its sole discretion, declare the entire unpaid balance of the loan immediately due and payable upon any such sale, transfer, lease, encumbrance, or disposition, or upon any change of ownership or occupancy of the Property, whether voluntary or involuntary.

- The Borrower will deliver to the Lender, upon request, any information, documents, or instruments that the Lender may require to protect or enforce its rights under this Mortgage Deed or the Note, or to verify the status and condition of the Property or the loan.

- The Borrower hereby assigns to the Lender the rents, issues, and profits of the Property, and authorizes the Lender to collect and apply the same to the loan, in the event of default by the Borrower or upon the commencement of foreclosure proceedings by the Lender.

- The Borrower hereby grants to the Lender the right to enter upon and inspect the Property at any reasonable time, and to take any action that the Lender may deem necessary or appropriate to preserve or protect the Property or the Lender’s interest therein.

- The Borrower hereby acknowledges that the Lender is relying on the representations and warranties made by the Borrower in this Mortgage Deed and the Note, and that any false or misleading statement or omission by the Borrower shall constitute a default hereunder and under the Note.

- The Borrower hereby agrees that, in the event of default by the Borrower under this Mortgage Deed or the Note, the Lender may, at its option, accelerate the maturity of the loan and declare the entire unpaid balance thereof, together with all accrued interest and fees, immediately due and payable, and may proceed to foreclose this Mortgage Deed by judicial or nonjudicial sale, or by any other method permitted by law, and may bid for and purchase the Property at any such sale, and may apply the proceeds of the sale, after deducting all costs and expenses, to the payment of the loan, and may recover from the Borrower any deficiency or surplus remaining after the sale.

- The Borrower hereby agrees to pay all costs and expenses, including reasonable attorney’s fees, incurred by the Lender in enforcing this Mortgage Deed or the Note, or in protecting or preserving the Property or the Lender’s interest therein.

- The Borrower hereby agrees that this Mortgage Deed and the Note shall be governed by and construed in accordance with the laws of the State of Illinois, and that any action or proceeding arising out of or relating to this Mortgage Deed or the Note shall be brought in the courts of the State of Illinois or the federal courts located therein, and that the Borrower hereby submits to the jurisdiction and venue of such courts.

- The Borrower hereby agrees that this Mortgage Deed and the Note contain the entire agreement between the parties with respect to the subject matter hereof, and that no oral or written modification or waiver of any provision hereof shall be binding unless signed by both parties.

- The Borrower hereby agrees that if any provision of this Mortgage Deed or the Note is held to be invalid, illegal, or unenforceable, the validity, legality, and enforceability of the remaining provisions shall not be affected or impaired thereby.

- The Borrower hereby agrees that the Lender’s failure or delay in exercising any right, power, or remedy hereunder or under the Note shall not operate as a waiver thereof, and that any single or partial exercise of any such right, power, or remedy shall not preclude any other or further exercise thereof or the exercise of any other right, power, or remedy.

IN WITNESS WHEREOF, the Borrower has executed this Mortgage Deed as of the date first written above.

John Smith, Borrower

STATE OF ILLINOIS )

) SS.

COUNTY OF SANGAMON )

On this 25th day of October, 2023, before me, a Notary Public in and for said County and State, personally appeared John Smith, known to me or proved to me on the basis of satisfactory evidence to be the person whose name is subscribed to the within instrument, and acknowledged to me that he executed the same in his authorized capacity, and that by his signature on the instrument, the person, or the entity upon behalf of which the person acted, executed the instrument.

WITNESS my hand and official seal.

Notary Public

My commission expires: _

Mortgage Deed Format Word

You can use the templates or samples that I found for you as a reference, but you should customize them according to your specific situation and needs. You can also create your own template from scratch, using the key elements that I mentioned earlier.

Mortgage Deed Format PDF

You can use the PDF format to save, print, share, or export your document. The PDF format preserves the layout, fonts, and styles of your document, and makes it easy to view and access on different devices and platforms.

Conclusion

A mortgage deed is a legal document that gives the lender a security interest in the property until the borrower pays off the loan. It contains the terms and conditions of the loan, such as the amount, interest rate, repayment schedule, and consequences of default. It also specifies the rights and obligations of both parties, such as the borrower’s right to use and maintain the property, and the lender’s right to inspect and foreclose the property.